SALES COMMENTARY

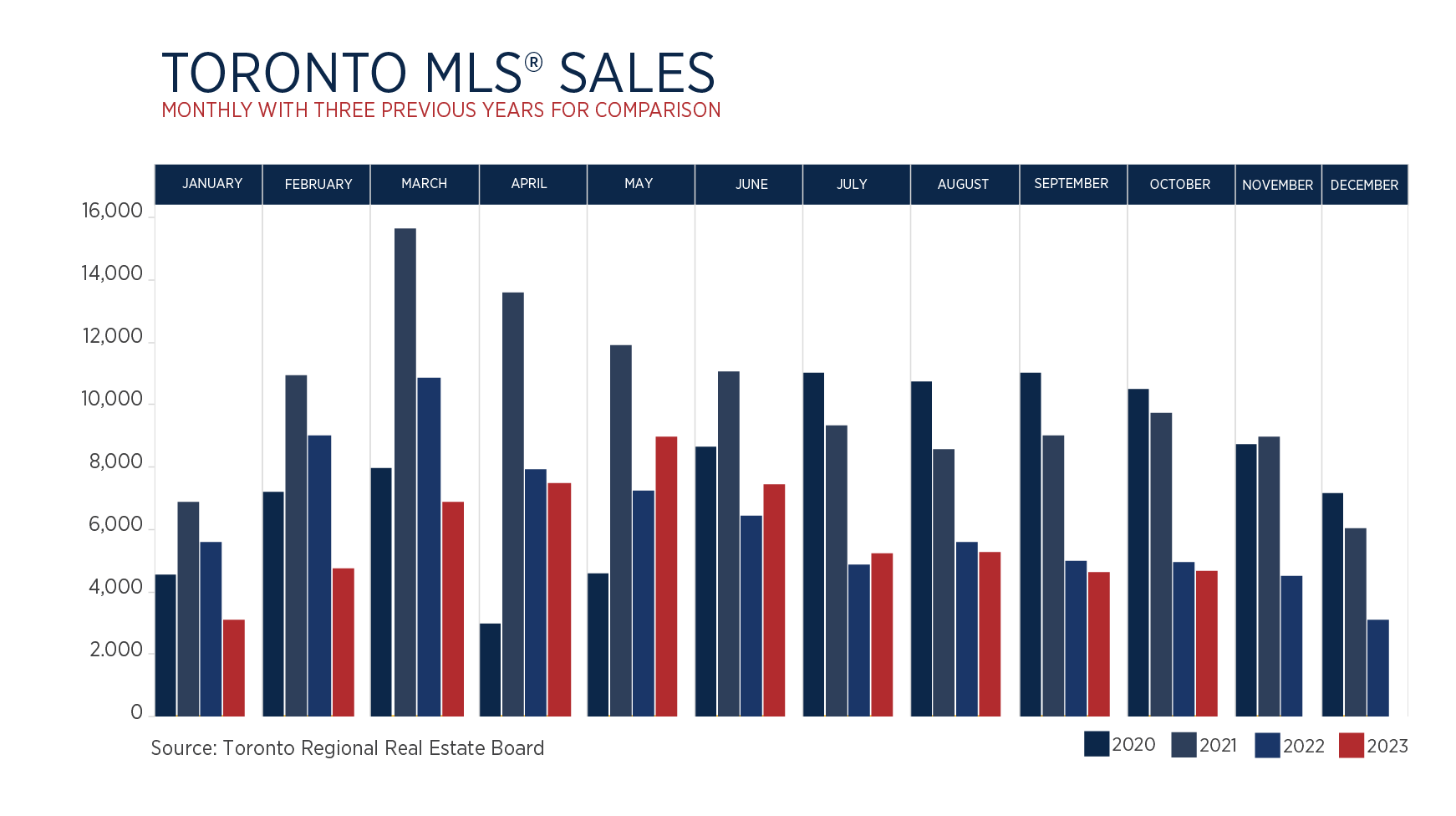

The good news for October was that sales on TRREB at 4,646 matched September levels. The bad news was that October sales were the lowest for this month since 1998! So where do buyers and sellers look for some positive signs?

The good news for October was that sales on TRREB at 4,646 matched September levels. The bad news was that October sales were the lowest for this month since 1998! So where do buyers and sellers look for some positive signs? First, it would appear that the Bank of Canada rates have plateaued at 5%. Everyone likes certainty. The bond market has since declined by 20-30 basis points which suggests that fixed rate mortgages may become cheaper. Looking further out, rates should start to decline by the middle of 2024.

Secondly, the sales-to-new listings ratio moved up from 28% last month to 32 % this month. But we are still in a ‘buyers market’. This occurred from an increase in listing cancellations, not from more buyers. For those with the money to buy, there are now some really good deals. You don’t have to worry about ‘multiple’ offers and you don’t have to worry about being rejected because your offer includes conditions.

Thirdly, there is another market for sellers. If you don’t get your price, then rent your property for a year. Rents are higher than a year ago and there are more tenants than usual – due to higher immigration and more people needing to rent.

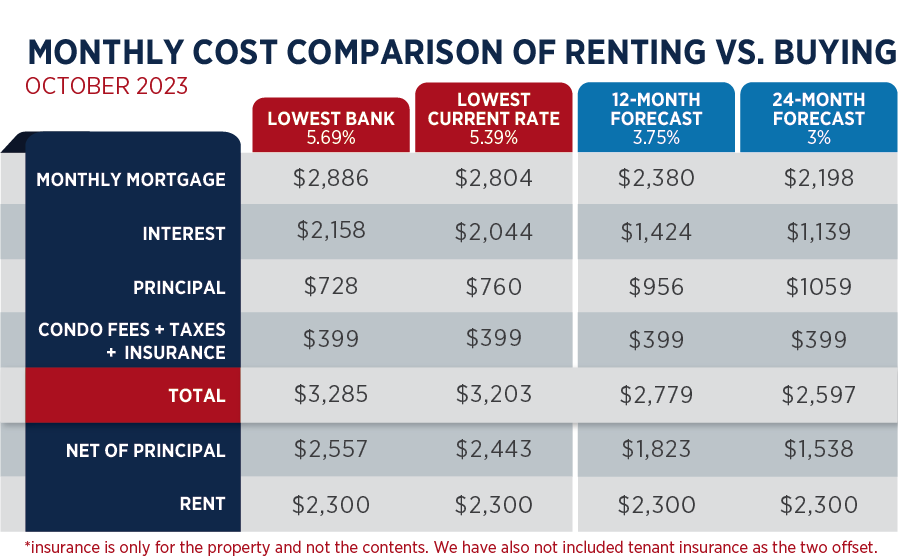

RENTING VS BUYING

What is the impact of interest rates in your decision?

The Table below shows the answers. While mortgage payments are critical to your cash flow, a portion of your payment is a repayment of principal. Starting with a 3.75% mortgage rate it is better to buy than to rent.

Now let’s compare what happens over the 5-year term. Assume all costs and rents increase at 2.5% per year. Your down payment was $23,500. If property prices increase by 2.5% as well, then your equity would increase by $61,000 before any principal repayment. That is equal to a monthly gain of $1,016 which would more than offset any cash flow deficits, even at today’s mortgage rates!

The conclusion: if you can afford today’s higher mortgage costs, it is still better to buy!

RENTAL COMMENTARY

In October, 1483 units were leased in the Downtown and Harbour Bay markets. This was down from the summer when 2500 units were leasing per month. The drop from September (1534) was minimal which indicates that more than just students are in the rental market. There are currently over 3,000 units available which represents a two-month supply. This has resulted in slightly lower rents and fewer multiple offer scenarios than last month.

This month we looked at two-bedroom units with one and two bathrooms. The available market for one- bathroom units is roughly 20% the size of the two-bathroom units. These tend to lease faster as the second bathroom adds almost $500 per month to the rent.

The table below represents average rents by bedroom type for October.